Add up the money in your bank accounts, insurance policies and homes. If you are like many Singaporeans, you could be a millionaire when you pass away.

Now if you do leave so much, could your children handle such a large amount of money so suddenly? From my experience, inheriting a large sum of money so suddenly can spell trouble. Your children could grow up feeling entitled, spoilt and not wanting to find a job at all. Or they could attract ‘friends’ who care only about your children’s wealth. Surely all this is not what you want.

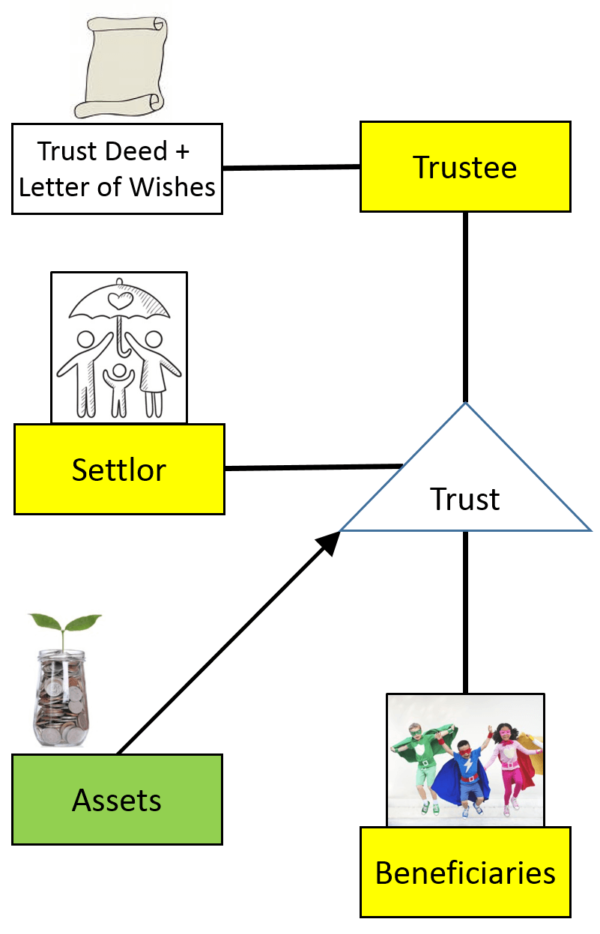

You May Need a Trust, Not Just a Will

What you need to consider is an instrument called a Trust. Use this article to understand what a Trust is by penning some thoughts down. Do leave your technical queries aside for now and focus on what you really wish to do.

Let’s Get Started

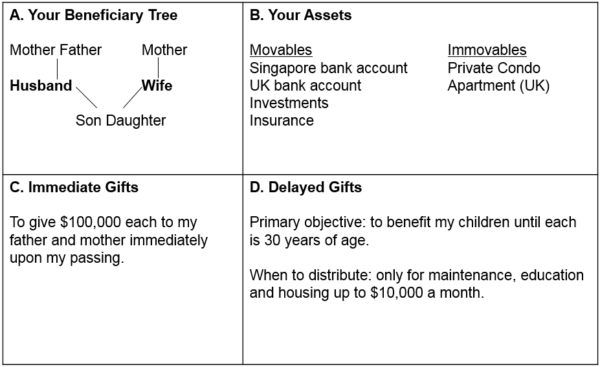

Divide a blank piece of A4-sized paper into 4 Quadrants as shown below. It’s already filled in with an example of Adam and his family.

Quadrant A – Specify your main beneficiaries

Here are the people that Adam (aged 45) wishes to benefit – Betty his wife (40), their two children (10 and 12), and his parents.

Quadrant B – List down your assets

Your assets can be divided into (a) immovables that “do not move” such as land and condos, and (b) movables that can move such as bank accounts and insurance policies.

Most of what Adam owns is situated in Singapore although he has a UK bank account and apartment.

Adam estimates his net worth at death (NWAD) is $3.2 million.

Quadrant C – Specify immediate gifts

Adam plans to give $200,000 to his parents and the remainder to be shared equally among his wife and two children. Should his children receive their gifts immediately upon his passing? I think that would be a bad idea. His children could become millionaires at a very young age and lose the desire to study and work thereafter.

Quadrant D – Specify staggered gifts

Adam decides to delay the gifts to his children by putting $2 million into a Trust which is really like a piggy bank. A person called a Trustee is then appointed to hold the money for his children over a period of time. Adam instructs the Trustee to release money to his children only for maintenance, education and medical expenses up to say $10,000 a month. Then when his children each reach 30, the remaining money can be given to them.

Conclusion

The simplified example above shows you the importance of considering both immediate and staggered gifts in your estate plan. Immediate gifts can be given away in a Will while staggered gifts are managed through a Trust.

Talk to us about your estate plan today.

If you are like most Singaporeans, you probably need a Trust, not just a Will.